The largest carry trade & unwind the world has ever... rewind?!

Let me start by acknowledging that bad is bad. Last week, there was a lot of panic in the market, and now the rates market expects the Federal Reserve to cut rates by 50 basis points in multiple meetings this year. The sentiment has shifted from expecting rates to go higher for a longer period to the possibility of seeing interest rates at 0 and quantitative easing.

In July, the labor market displayed signs of weakness as only 114,000 jobs were added, falling short of the anticipated 175,000. This unexpected shortfall led to an increase in the unemployment rate to 4.3%, which triggered the "Sahm recession rule" due to jobless claims rising more than expected.

What is the Sahm Rule recession indicator?

The Sam recession indicator, also known as the Sahm Rule, is used to anticipate the beginning of a recession in the United States. Claudia Sahm, a former economist at the Federal Reserve, created it.

The Sahm rule indicates the start of a recession when the 3-month moving average of the national unemployment rate rises by 0.5% or more from its lowest point in 12 months. The rule uses unemployment rate data published by the U.S. Bureau of Labor Statistics (BLS).

Historically, the Sahm rule is one of the most accurate indicators to predict a recession, with a solid track record of only being wrong once.

However, Claudia Sahm, the creator of the Sahm Rule Recession indicator, commented

The Sahm rule is likely overstating the labor market's weakening due to unusual shifts in labor supply caused by the pandemic and immigration - https://stayathomemacro.substack.com/p/sahm-thing-more-on-the-sahm-rule

However, as someone in my Discord pointed out, she might be saying it to cover her ass as it might not work this time, just in case. Then, she can always say that she made a statement. I wouldn't want to be blamed by so many people relying on an indicator I wrote myself.

Discord link?

Currently, I am not accepting new Discord members. There are some problems with Ghost blog new API. I created a Discord bot but their new API changes made most API calls obsolete and the way of creating private calls with JWT tokens.

As the market turned, big institutions, hedge funds, banks, etc., demanded rate cuts. Overall, the labor market is cooling without collapsing, which aligns with what the Federal Reserve wants.

What is the carry trade?

A "carry trade" strategy involves borrowing money in a currency with a low interest rate and then using the borrowed money to invest in a currency with a high interest rate.

The trader "carries" the trade from the low-interest rate environment to the high-interest rate environment.

The yen (JPY) is the low-interest-rate currency. Investors would borrow yen because it's cheap to do so (thanks to the interest rate set by the Bank of Japan).

The U.S. Dollar (USD) offers higher interest rates. Investors would then convert the borrowed yen into dollars and invest in dollar-denominated assets like bonds, offering higher returns.

The idea is to profit from the difference in interest rates between the 2 currencies. If you're borrowing at a 0% rate but investing at a 2% rate, you'd earn the difference (minutes transaction costs)

The Carry strategy can be even more profitable if the high-interest-rate currency (USD, in this case) appreciates against the low-interest rate (JPY). That's because when you close the trade, you would convert to the yen at a more favorable rate.

However, the carry trade in USDJPY offered around multi-year highs in terms of returns.

Sounds familiar? Ms Wattanabe, the real housewives of Japan

You can't unwind the largest carry trade the world has ever seen without beheading a few

The process of unwinding the largest carry trade in history is not without its difficulties, and we're witnessing some negative effects. Markets have been reacting to a series of weak economic indicators from the U.S. The latest labor market report showed signs of weakness, adding to worries after a disappointing ISM survey hinted at a slowdown in economic activity. This has created uncertainty and triggered a significant market reaction.

Will the Federal Reserve alter its approach due to these signs? How will global markets, already sensitive to shifts in the U.S. economy, react?

Monday morning market moves should be taken with a grain of salt since they often happen in a vacuum. As of the time of writing, we can tell that we are waiting for the ISM data. The consensus expects a bounce to 51 from last month's 48.8, but the real consensus is a bit lower after last week's reports.

If the data comes in as expected, the overnight weakness in risk assets might be mostly reversed by the end of the day. However this might not really change the shift in sentiment.

Edit, during the time of writing this article, the data got released

Perhaps the larger risk now isn't what the FX market does but what happens with equities, especially tech stocks. We've seen a massive rally and stretched valuations, and Warren Buffet's preference for cash is grabbing headlines. However, the labor market is still tight, but if stocks fall too far or too fast or if the August jobs report, released at the start of September, turns out weak, things could get uglier. I still expect a series of Fed speakers hinting at a 25 bps rate cut next month.

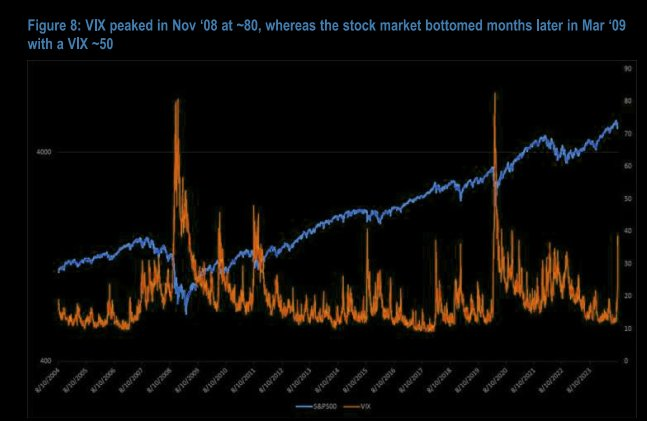

VIX and SPX500 correlation

Lately, stock market indexes have experienced significant declines, causing increased volatility and a rise in options prices. Normally, there is a relationship between the VIX and SPX500. However, when market volatility suddenly increases, this correlation becomes less predictable. The unpredictability is influenced by the behavior of VIX Exchange-Traded Products (ETPs), which begin to have a more pronounced impact.

VIX ETPs track the VIX index and are categorized into long and short ETPs. When the VIX rises, both types of ETPs rebalance their position by buying VIX futures. This amplifies movements to the upside in the VIX, especially during market close.

On Monday, the VIX and VIX futures experienced a sudden increase in pre-market trading, possibly due to VIX ETPs increasing their buying activity. However, the direct impact of this buying was not immediately evident and only became noticeable at the market close. Nevertheless, the market was able to absorb these effects without a significant disruption.

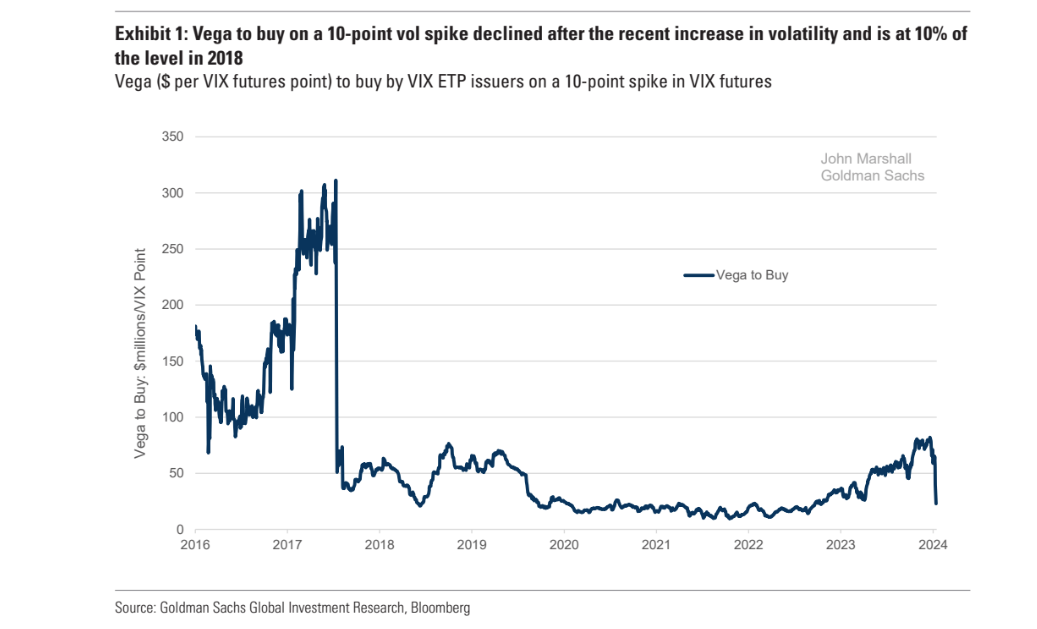

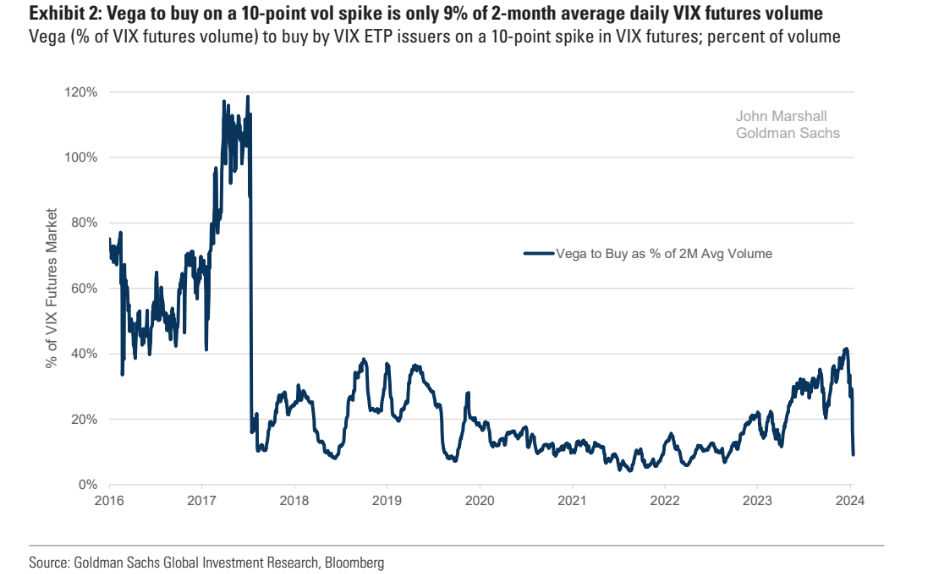

Before the market opened on Monday, Goldman Sachs projected that a 10-point increase in VIX futures, specifically the average of the August 2024 and September 2024 VIX futures, would result in 40 million VIX futures by VIX ETPs. This amount represents 15% of the volume seen at the peak in January 2018, just before the VIX spike in February 2018.

After the 1-month VIX future rose by 8 points, the buying pressure weakened. If VIX futures were to go up by 10 points, VIX ETPs would likely buy about 23 million VIX futures, which is approximately 9% of the average daily VIX futures trading volume.

The risk of a technical VIX spike has decreased as the number of VIX futures owned by long-VIX exchange-traded products (ETPs) has increased compared to short-VIX ETPs. GS estimates that Long-VIX ETPs now hold 1.2 times more VIX futures than short-VIX

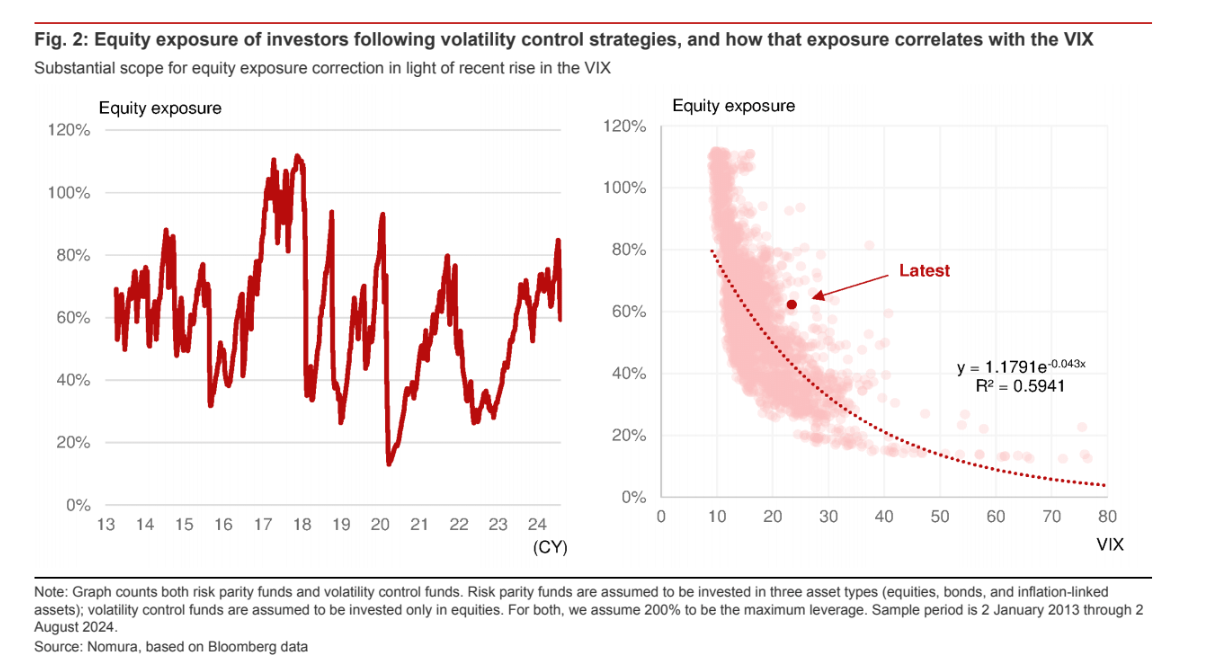

Funds often rely on "volatility control strategies". On the right side, we have a scatter plot that tells another intriguing story about how equity exposure correlates with the VIX.

he dotted red line illustrates an exponential decay trend, meaning as the VIX goes up, equity exposure tends to go down. Obviously, when the market isn't doing well, investors often pull back to reduce risk.

The marker on the plot points to a recent decrease in equity exposure, corresponding with a rise in the VIX. This matches the historical pattern and shows that investors are actively adjusting their strategies in response to increased market volatility.

The data considers both risk parity funds (which diversify across equities, bonds, and inflation-linked assets) and volatility control funds (focused solely on equities). These funds assume a maximum leverage of 200%.

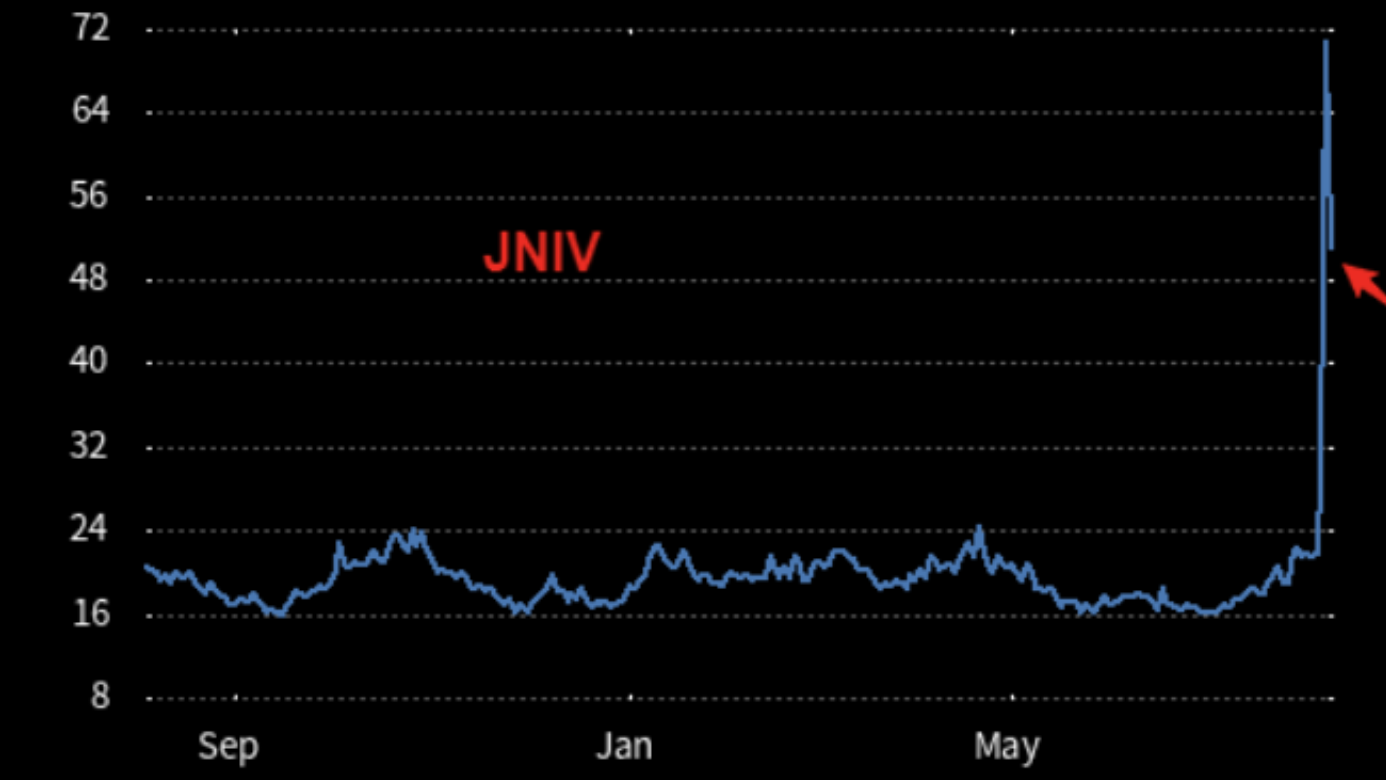

Also here is the Nikkei VIX

According to JPMorgan

The market doesn't bottom when the VIX peaks. Instead, markets are more likely to bottom after the VIX starts to fall. Market often finds its bottom when the VIX has fallen about 1/3 of the way back toward its normal levels

Nasdaq

EDIT: JUST IN

BoJ’s Uchida: We won't hike rates when markets are unstable

On the one side, I can't even write an article without major news coming in. On the other side, this is hilarious. Now after the big unwind of the carry trade, BoJ capitulates

I will see tomorrow what further news comes in that changes everything 😆