Why I am investing in Meta

Many still associate Meta exclusively with Facebook. I used to be one of those people until yesterday. Yesterday, I was at the dentist but decided to buy META on my phone when I accidentally bought 100x more shares than I was supposed to. This was needed for me to see the light.

You may see this as an accident; a simple spot buy turned into a full stock position on margin, which has to be closed. To me, this was divine intervention.

Meta Q4 2024 earnings will be released soon, and I am optimistic. A major factor behind optimism is Meta's strategic investments this year, which can shape expense and capital expenditure (CapEx) guidance while setting the stage for compounding earnings growth through 2027.

Meta jacked up their investments in high-performance compute infrastructure and open-source projects. These investments aren't cheap, but this is how Meta can stay ahead or at least not fall behind the curve.

While the payoff doesn't qualify as instant gratification, it can definitely boost Meta's earnings potential in the coming years—or at least make the crowd believe earnings will be good.

I can definitely see Meta's share price going up another 13% - 17% from here. So that would be a price of $685 - 690.

There's a strong demand for existing ad products such as Reels. High adoption for new AI-driven solutions like Advantage+ and expansion of click-to-messaging ads and possibly paid messaging solutions.

Advertising is still Meta's main source of income but they want to stay ahead of competitors. By investing in AI & AR/VR, they can develop new services and products that can bring in more money over time.

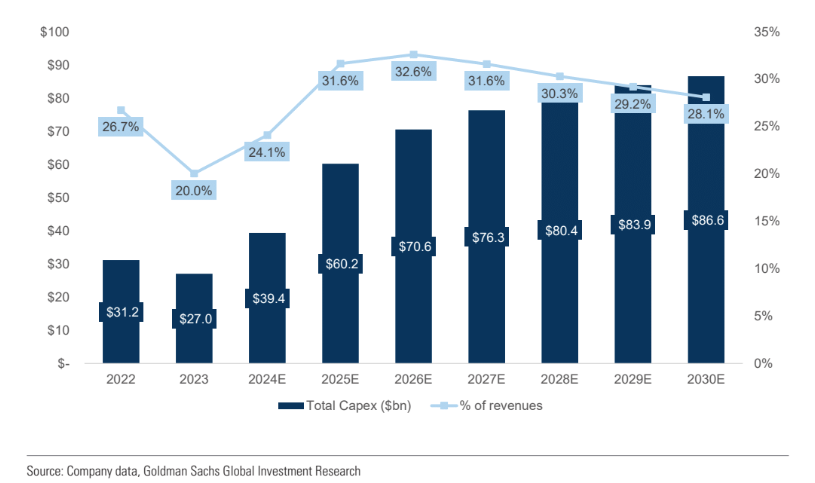

GS estimates for 2025, that Meta will spend $116.1 billion, 19% more than in 2024, including all costs related to running the business. For capital expenditure, there is an estimated $60.2 billion on long-term projects, a 53% increase compared to 2024.

Reels monetization

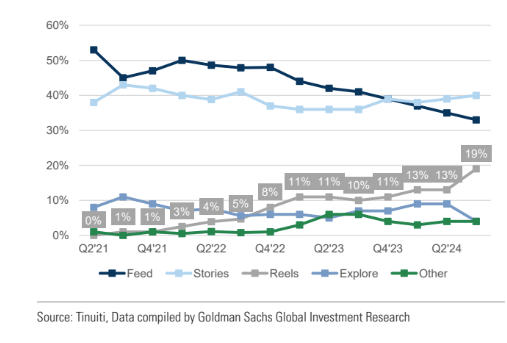

Reels, Meta's short-form video format on Instagram and Facebook is exploding in popularity. By monetizing reels into a format that consumers and advertisers already like while keeping users engaged on Instagram and Facebook.

People are spending more time on Reeds, as shown by daily usage data like SensorTower's stat, making it an area to focus on monetization.

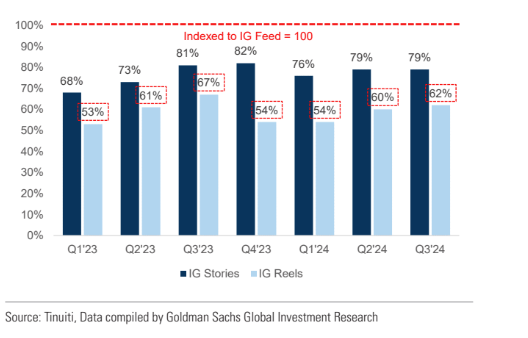

Although Reels achieved "revenue neutrality" by the end of 2023, meaning its revenue now offsets the associated costs, this doesn't mean Reels has fully matured as a revenue stream.

More advertisers are starting to use Reels to reach audiences, especially for tools like Advantage+ (a generative AI platform that helps create ads). Reels ads are still cheaper than traditional Instagram and Facebook feeds or stories ads. For example, the cost per thousand impressions (CPM) for reels is about 38% lower than Instagram feed ads. As more advertisers see the value of Reels, pricing for these ads is likely to increase, boosting revenue.

Data shows that Reels accounted for only about 19% of ad impressions on Instagram in Q3 2024. There's still room for growth. With CPMs for Reels lower than other ad formats, advertisers can get a lot of value here.

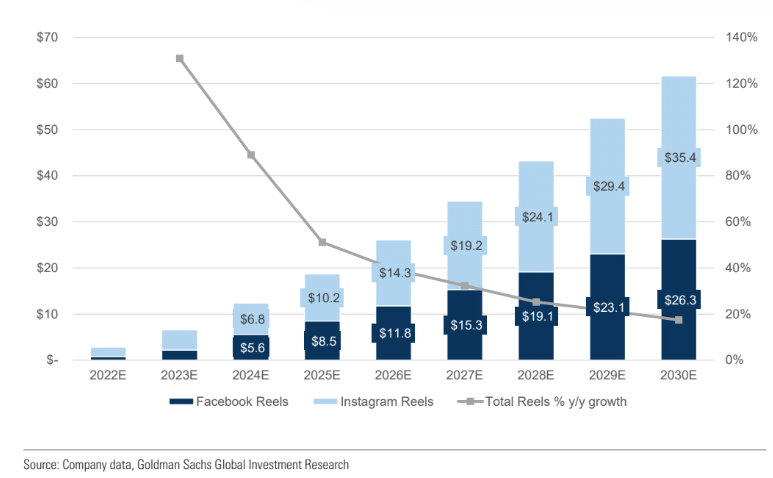

GS forecasted to grow Reels revenue at a compound annual growth rate of ~59% to 2026. By 2026, Reels is expected to bring in $26 billion in revenue across Facebook and Instagram, making up 12% of Meta's total advertising revenues.

Advantage+: Meta’s AI-Powered Growth Engine

Advantage+ is a generative AI platform that helps create ads and optimize campaigns. Advantage+ uses AI to handle ad targeting, placement, and conversions, which helps businesses (especially smaller ones) get better results without needing an in-house marketing team.

Advantage AI+ lowers the entry bar by automating campaign creation with generative AI for ad creatives. This is great for small and even medium-sized businesses that don't have the time or resources to develop a complex ad strategy.

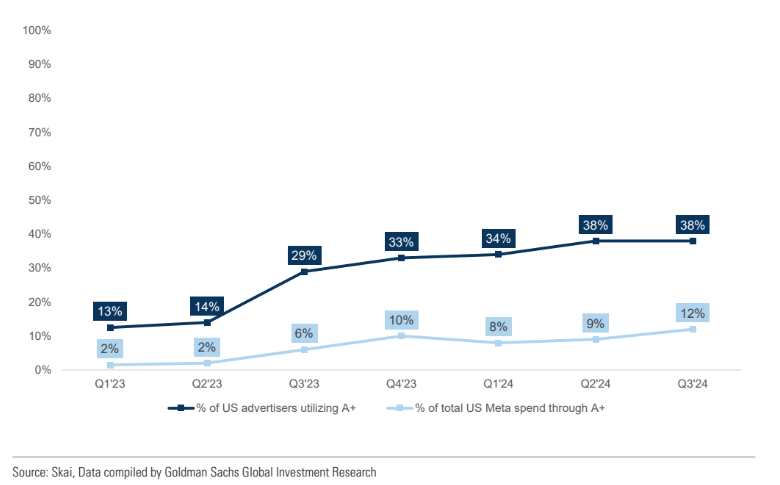

According to data, only 38% of U.S. advertisers used Advantage+ in Q3 of 2024, with just 12% of total Meta ad spend flowing through the tool. However, there's still a lot of upside, as many advertisers still need to discover how these AI-driven features can streamline their campaigns and boost ROI.

Meta's generative AI creative tool, part of the Advantage+ suite,, has already attracted over 1 million advertisers since its December 2024 rollout. However, that's still less than 10% of Meta's 10+ million total advertisers. There's still a log of upside.

Messaging

Messaging could be one of the biggest but least explored opportunities for Meta, such as Click-to-message Ads and paid messaging.

Click-to-message ads let users immediately jump into a conversation on WhatsApp, Messenger, or Instagram DM.

These ads look like regular posts or sponsored content in Facebook and Instagram feeds or stories. Instead of a "Shop now" or "Lean More" button, they have a button like "Message Us" or "Chat on Whatsapp".

When users click the button, they're directly taken to a messaging app such as WhatsApp, messenger, or Instagram direct messages to start a conversation with the business.

When users click the button, they're directly taken to a messaging app such as WhatsApp, Messenger, or Instagram direct messages to start a conversation with the business. These ads let businesses have direct conversations with potential customers. They can help users answer questions, provide service, or complete a purchase. Ads turn into a direction communication tool. Customers like them because they can get instant answers without the need to email or visit a site.

By the end of 2022, Meta said these ads hit a $10 billion annualized run rate, with click-to-WhatsApp ads making up a multi-billion dollar chunk. By Q1 2024, paid messaging topped a $1 billion annualized run rate.

Meta's messaging revenues (click-to-message + paid messaging) could climb at a ~29% compound annual growth rate until 2026, hitting around $23.8 billion in 2026. To put that in perspective, that's about 11% of total revenue from Meta's Apps such as Facebook, Instagram, Whatsapp, and Messenger.

Long-Term growth bets

While advertising is still Meta's main source of income, they're busy finding ways for several long-term revenue opportunities.

Meta's AI, with sponsored search results, integrates AI into chat while offering targeted sponsored content that feels more organic.

AI agents, think about AI-driven virtual assistants that handle customer service, marketing tasks, etc. These tools for creators and businesses can potentially become a paid subscription.

Meta wants to be a leader in AI, whether that's better for algorithms serving ads or chatbots for businesses. Meanwhile, Reality Labs is Meta's bet on the future of virtual and augmented reality. This includes hardware like Quest VR headset, Ray-Ban smart glasses, and platforms where users can interact, work, and play in immersive 3D environments.

Remember the Llama AI model. Even though Meta has taken an open-source approach so far, there's talk that it could one day license its AI tech for enterprise use, similar to how openAI's GPT or Google Gemini/Vertex AI works.

It's tough to make confident revenue forecasts. While there's a real upside, it might be possible some of this hype is "priced in" to a certain extent, despite it being too early to tell how adoption will happen or how these offerings will influence business models over time.

TikTok Litigation

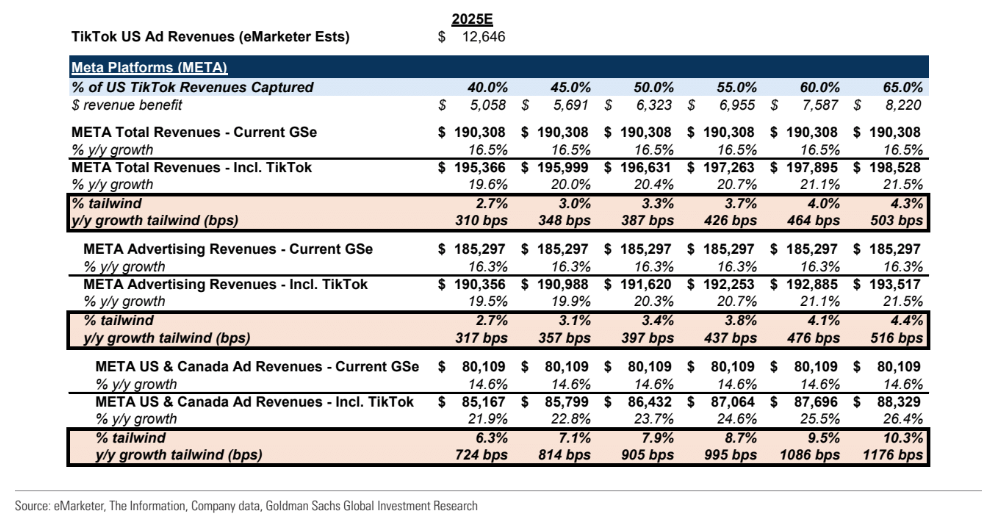

It's also important to track TikTok's US litigation and the Protecting Americans from Foreign Adversary Controlled Application Act. It will be interesting once TikTok's US operations are fully shut down.

Think about how much US ad revenue TikTok currently pulls in and how that spend might be reallocated among other ad players like Meta, YouTube, Snapchat, Pinterest, and Reddit if TikTok is forced out of the market entirely.

If advertisers have budgets earmarked for TikTok and suddenly need to place them elsewhere, Meta's platforms could see an influx of ad money.

The bottom line is that ongoing litigation could open the door for a wave of ad spending to flow to Meta if TikTok faces a ban or major restrictions in the US market.

Meta is putting money into its AI infrastructure, data centers, and Reality Labs for augmented and virtual reality (AR/VR) development. Goldman Sachs predicts that Meta's total capital spending will grow by an average of 38% each year from 2023 to 2026. By 2025, this spending could reach $60.2 billion, which is a 53% increase compared to 2024.

All this spending will eventually show up as depreciation cost (spreading out the cost of investments over time) which is expected to grow even faster than capex at 41% per year

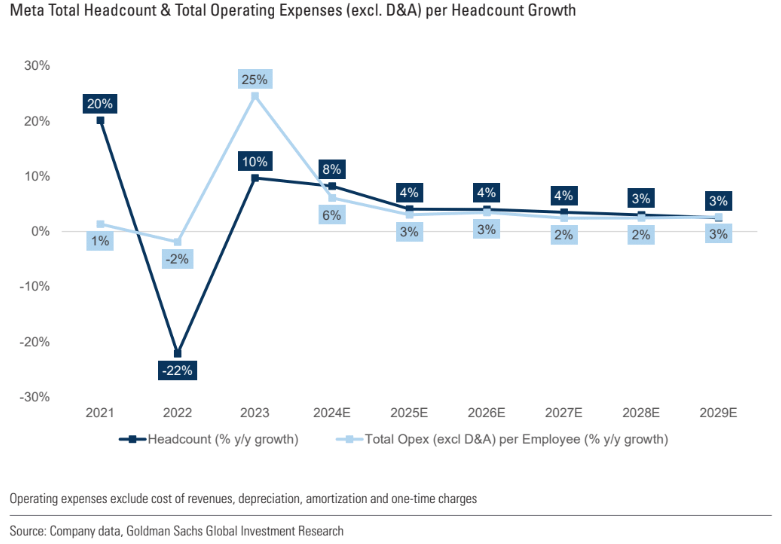

They plan to control other operating expenses, such as salaries and day-to-day costs, over the next three years. Headcount will also be modest, with management focused on hiring specialized, higher-paid roles.

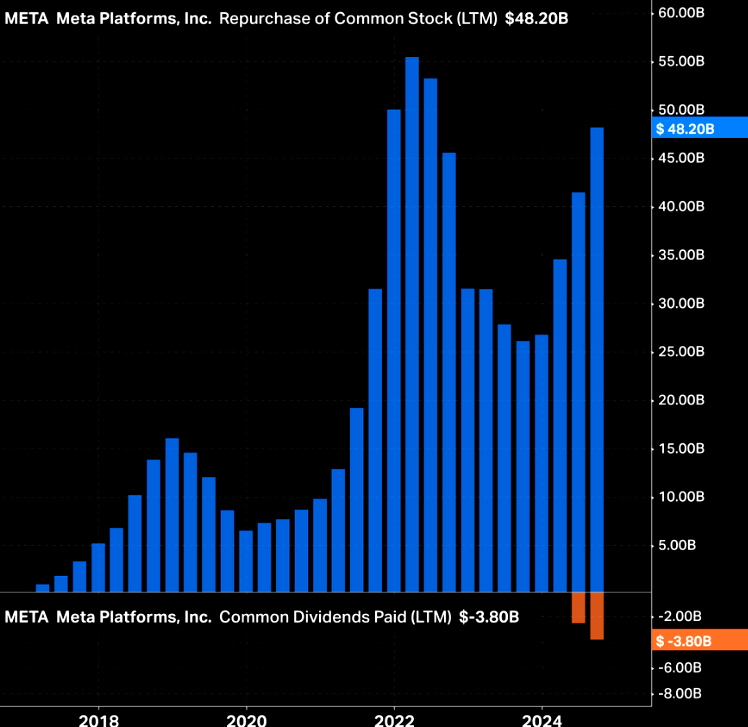

In 2018, Meta paid about $5 billion to its shareholders each year by buying back its own shares. Over the past 12 months, Meta ramped up these returns:

- $48 billion spent on share repurchases.

- $4 billion distributed as dividends (direct payments to shareholders)

In the past year, Meta has returned $52 billion to its shareholders. This amount is much higher than what it gave back in 2018.

Shareholder returns through buybacks and dividends show confidence in long-term profitability. This is a clear sign that Meta has excess cash to reward investors, even as they continue to invest in initiatives like AI and Reality Labs.

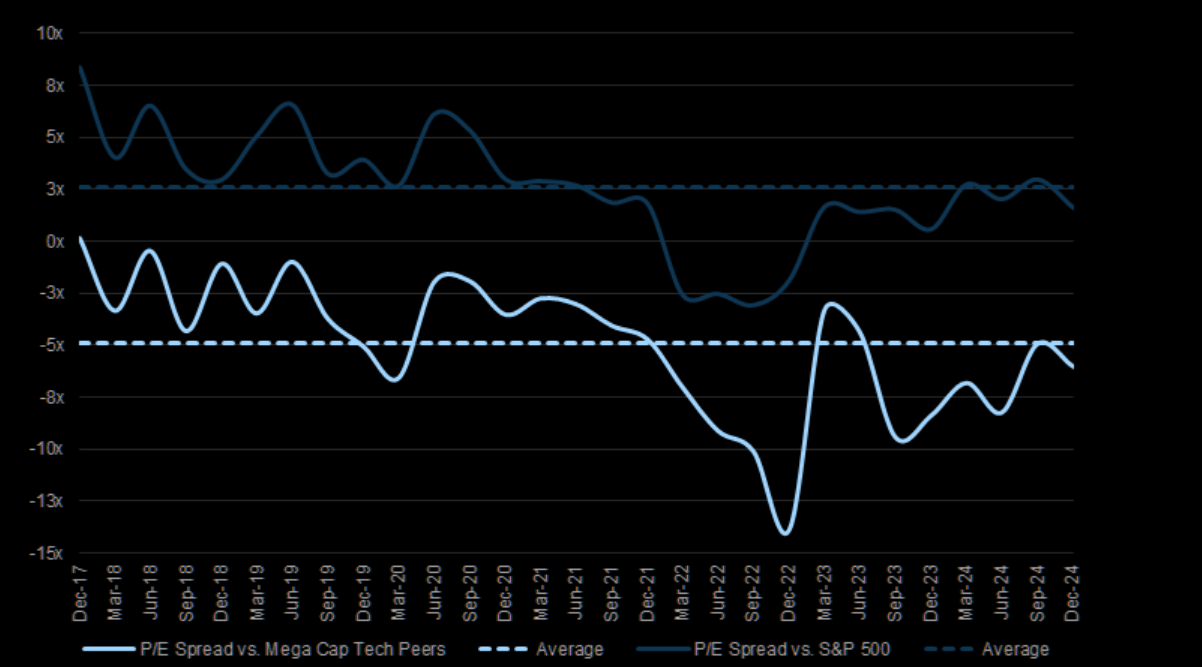

META's current valuation seems reasonable. It is trading at about 22 times its estimated GAAP earnings per share for 2026, similar to the S&P 500's 21.5 times. Additionally, META is priced lower than its peers, which include GOOGL, MSFT, AMZN, AAPL, and NVDA.

Also, if you are a premium member, join Discord for full benefits.

Yes, options data, such as dark pools, options gamma, unusual flow, etc., are also included.