Global equity newsletter: "The Neoliberal Era Killshot" 18-07-2024

First of all, before looking at the markets, let's go over what happened over the weekend. Over the weekend, during a bustling rally in Butler, Pennsylvania, Donald Trump faced a near-fatal shot. A shooter, concealed on a nearby rooftop, targeted Trump. A gunshot echoed, and a bullet grazed Trump's ear, drawing blood. For a moment, we saw our candidate duck to the ground.

I will say this will be a shorter article because I am busy with trading now. I have been active a lot in Discord and posting stuff. Yet, I didn't have much time to write in May and June due to being busy with via 2.0 and traveling to meet up with my team. This article will be shorter than my usual 20-40-minute reads. My writing right now is not at its best since I am a bit disracted with the markets but hey, let's do it

But in a move defining his campaign, Trump regained his composure and raised his fist in the air—a defiant gesture that would soon become legendary.

His secret service team quickly moved in, whisking him to safety. A sharp-shooting Secret Service sniper took the attacker down, but the ordeal was far from over. Unfortunately, an innocent bystander lost his life, and stray bullets critically injured two others. Trump was rushed to a hospital, where doctors confirmed he was unharmed. Calling this a miracle would be an understatement.

From the Oval Office, Biden condemned the violence. However, he also stated that we should "not assume the motive of the killer."

Donald Trump arrived in the city on Sunday ahead of his expected confirmation as the Republican Party’s nominee for the Presidency. His keynote address was on Thursday, and Trump was also expected to announce his choice.

(VP will be Vance; news dropped before publishing this article)

As the week began, there was widespread speculation about who Trump would choose as his running mate. The odds increasingly favored Ohio Senator J.D. Vance, a strong advocate of the MAGA brand of conservative nationalism.

What happened over this weekend has a historical echo in the attempted assassination of President Reagan in 1981. At the time of Reagan's shooting, the 'Reaganomics' policy of neoliberalism was in its early stages and subsequently became the dominant economic policy for the next 40 years.

The attempted assassination of Trump could mark the end of this neoliberal era, as the world appears to be shifting back towards economic nationalism characterized by protective tariffs and tighter controls on the international movement of labor and capital.

Off the record, there are rumors among the House Democrats that they now anticipate a second Trump presidency. The question remains whether there will be a complete Republican sweep of Congress and the presidency.

Financial markets are already adjusting to a "Trump trade," yet we don't know the potential consequences. Simultaneously, the White House is shifting towards a more populist approach in its electoral strategy. Biden proposed capping rent increases at 5%, though the mechanism for implementing this remains unclear.

Equity markets

Yesterday, equities were weaker across the board. Yields remain stable, but the dollar reversed back lower, along with bitcoin, altcoins, and Gold. Last night, there was mixed price action as Japan Tech dropped notably, pulling the broader Japanese market down.

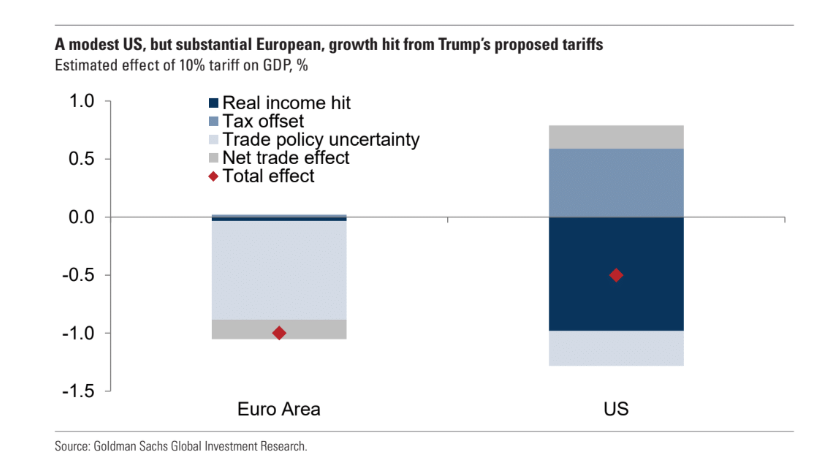

Europe outperformed the US, which was surprising given the headlines about trade restrictions. The Biden administration's recent trade-related announcement brought back attention to the potential impact of Trump's tariffs. Goldman Sachs GIR estimated a 1% reduction in Europe's GDP if the US imposes 10% tariffs on imports.

ASML, which is 10% of the SXE5, dropped more than 10%, having its weakest session since March 2020, along with 2 other major stocks. One of these stocks, Novo, dropped by 5% due to rival company Roche's release of obesity drug data, which pulled down the overall SXE5 performance. There were struggles in the US in tech stocks, with Nvidia leading the broader drop of the Nasdaq.

I am holding ASML. Well, my portfolio needs a lot of adjustments before Trump becomes president. Trump's statement that he won't defend Taiwan definitely temporarily damaged my portfolio. The stock market panic spilled over into Bitcoin.

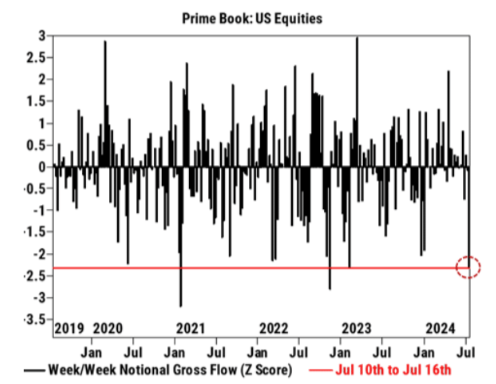

Recent sessions have seen a rotation with heavyweights weakening. Yesterday, this momentum unwind was pretty harsh. The GS momentum factor dropped by 2.5 standard deviations, resulting in fundamental long/short managers experiencing their worst day since the end of 2022.

Despite significant hedge fund de-grossing in US Tech in June, which continued into this month (the largest de-grossing since November 2022, which was also the bottom at the time).

Tech is difficult to choose—buy or not? With earnings still over a week away, there is no specific event to divert attention from macroeconomic concerns. On the macro side, comments from Fed Williams and Waller yesterday resulted in the market reassessing expectations, reducing the likelihood of a July rate cut, and focusing more on the possibility of a cut in September.

I think the Fed will keep the current Fed funds rate range of 5.25-5.5% with a first 25bps rate cut in September at least and another rate cut in December. The ECB will probably follow with a 25bps cut in September.

Discord link?

Currently, I am not accepting new Discord members. There are some problems with Ghost blog new API. I created a Discord bot but their new API changes made most API calls obsolete and the way of creating private calls with JWT tokens.

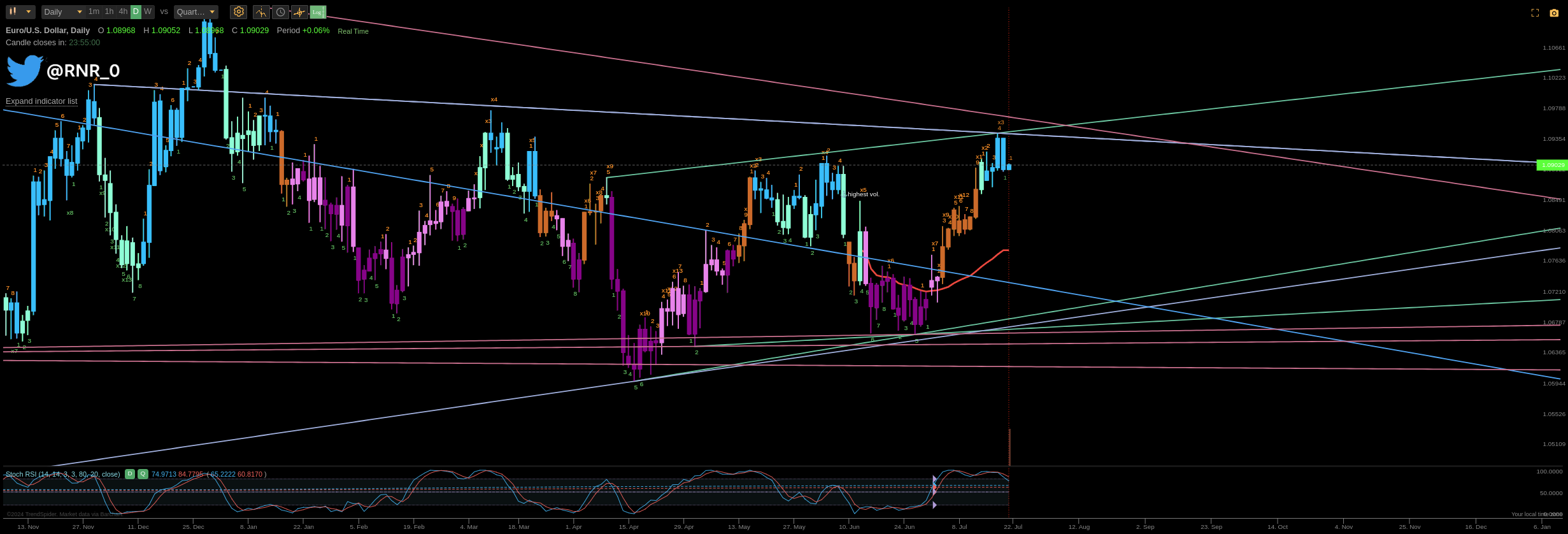

FX

Some small FX charts, I didn't look at rates yet, so take these all with a grain of salt.

AUDCAD signals of exhaustion

EURUSD, I wouldn't say I like it. It seems a bit of a local top. I hope I am wrong on this one.

Trump

So, back to Trump. The chance of Trump winning increased, and beating markets followed. If Trump wins, it could majorly affect the economy and markets, especially around trade policies and tariffs.

If Trump implements a 10% tariff on US imports, it would impact US economic growth slightly. Still, it could really hurt the Euro area because Europe's economy is very sensitive to changes in trade policies. Higher US tariffs would probably make the dollar stronger.

Trump discussed the possibility of devaluing the dollar while increasing tariffs, similar to the events of the 1971 Smithsonian Agreement. However, a major coordinated currency agreement is unlikely due to varying macroeconomics and institutional and logistical challenges.

In the equities markets, big tariffs would likely help US companies that make money and source domestically compared to those that rely on international markets. In Europe, a 10% US import tariff could cut earnings per share by 6-7%; however, companies with a lot of US exposure and some defensive stocks might perform well if Trump gets re-elected.

In addition, Trump's potential deregulation could boost big tech stocks. Under his administration, the corporate bond market and bonds from banks and tech companies will probably also gain.

Low vol summer?

As a reminder, Nomura securities analysts think equities will reach new highs in 2024, influenced by a "low-vol summer melt-up" before the elections.

Options sellers constantly supply volatility. These options sellers are focused on volatility premium harvesting. The cooling of US economic data suggests the market expects the Federal Reserve to cut rates multiple times before the end of 2024.

Now, here's the Trump card. The chances of Trump winning the election are growing; the market believes this could boost future growth. However, still be careful. There's also a chance for Vol upside, but this might not happen until after the election.

Here is what worries me personally

First, if new fiscal stimulus measures are introduced, they might worsen the government's deficit. This could lead to the need for the government to refinance its debt, creating risks related to Treasury refunding in late Q4 2024 or early 2025.

To manage the deficit, the government may decide to issue more bonds, which could lead to an increase in long-term interest rates. If Trump's policies cause economic growth and inflation, it could also hinder the Federal Reserve's efforts to lower interest rates.

The combination of fiscal stimulus increased debt issuance and growth-stimulative policies might lead to higher volatility and slower reductions in interest rates after the elections.

However, is it the top of everything right now when SPX500 has had the best Sharpe ratio? Usually, it ends with retail mania. I see Bitcoin at the bottom. Back at the end of 2021, it was at the top.

Yes, I, too, am disappointed. Summer is coming to an end, and without altcoin summer. At least Gen Z enjoyed Solana meme token summer (which usually ended with a rug but don't look a given horse in the mouth)

Blablaba pls sir any calls I can act on?!

Apple (AAPL) 12-month price target: $265 Current price: $223.90 Expecting Apple to deliver another EPS beat in Q3 2024. At the same time, iPhone revenues are falling due to a recent price discount to clean up their inventory and attract customers.

While iPad revenue should double for the new iPad models launched, such as the iPad Pro M4 and the iPad Air with the M2 chips.

Expect revenue to increase with their current sales on MacBook M3 while wearables (watches, etc.) drop. Service revenue grows due to strong app store spending. Also, there are opportunities for price increases in the new iPhone.

They haven't done that since 2020, but given their investment in hardware, iOS, and component cost inflation, There's a chance for a price increase. They also plan for thinner phones (god, they're making progress for once here). GS expects revenue to rise by 13% YoY.

Also, apple AI, Walmart partnership, and some other new "tech" they're releasing, including MacOS Sequoia with writing tools, image generation, etc. However, their current discounts are giving us a bit of a headwind but also providing us with dips as they try to clean their inventory.

I am buying Apple stocks during this dip today and tomorrow at the current price of $224, with a long-term target of $265.

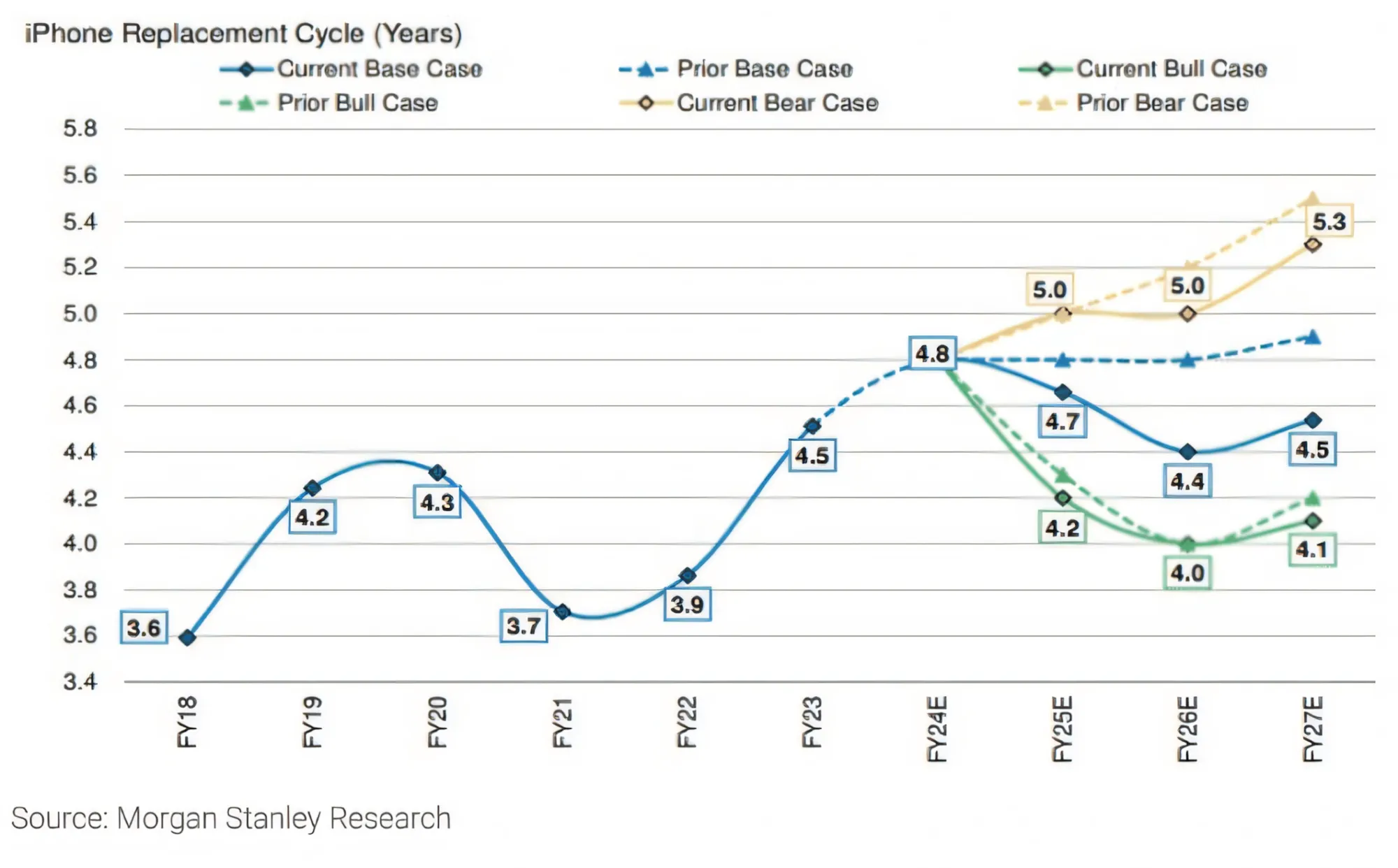

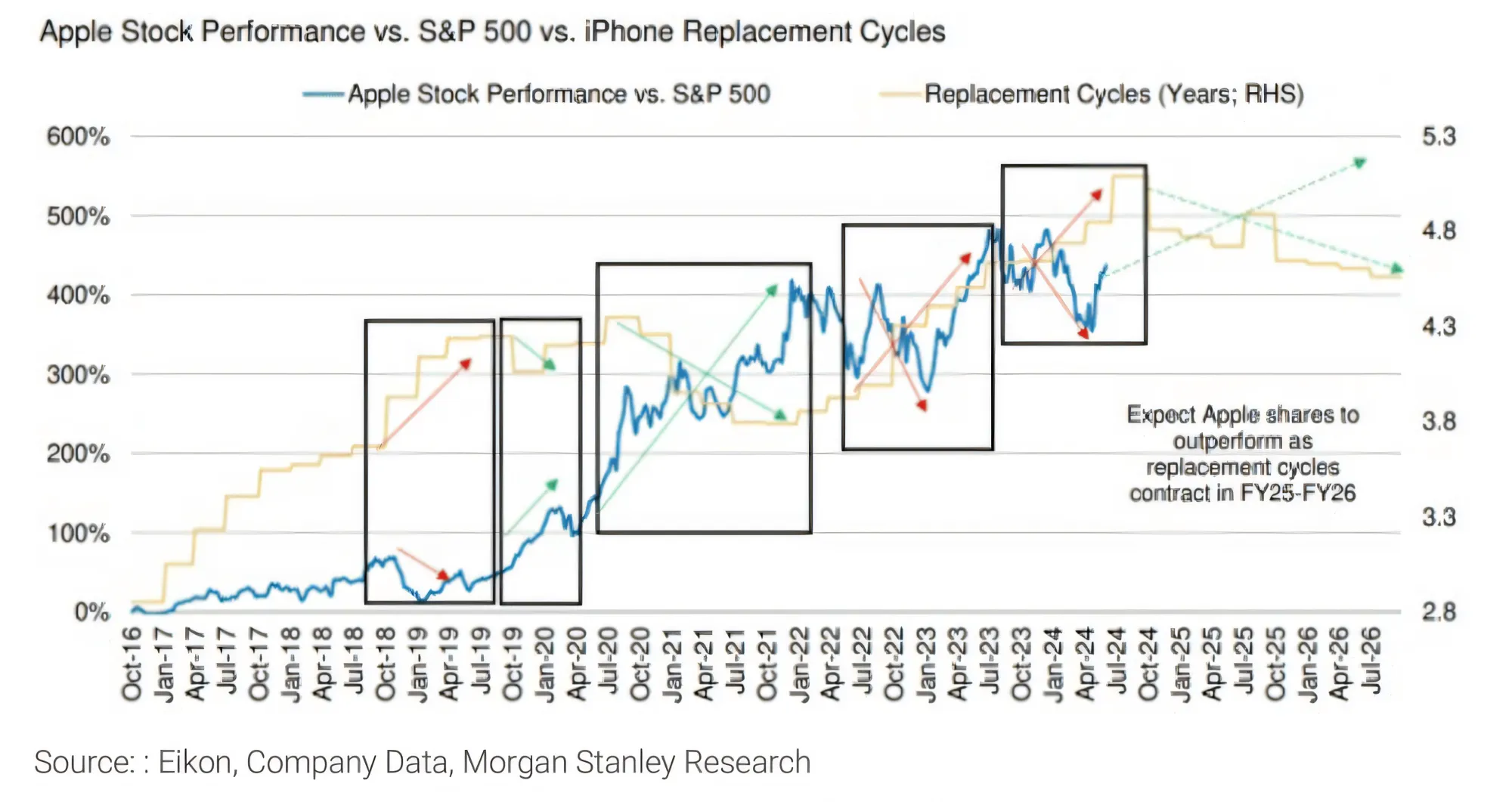

Meanwhile, Morgan Stanley believes Apple Intelligence will likely spark record smartphone upgrade cycles. Which I totally understand, and this might be a genius of Apple.

The new "AI smartphone Era" will come with the official launch of Apple Intelligence. While this launch can accelerate Edge AI development in smartphones and more transformative applications within 1-2 years (which all sounds great) but guess what? Your iPhone will be obsolete faster than before with every new iPhone launch.

Morgan Stanley forecasts that the iPhone replacement cycle will shorten by 0.1 years year over year in 2025 to 4.7 years and by another 0.3 years year over year in 2026 to 4.4 years. Historically, Apple shares have outperformed during periods of contracting replacement cycles.

Another one? The big rotation

In this chart, you can see the 5 major industry sectors, which are Consumer Staples, Utilities, Healthcare, Telcos, and Tech. You can see the largest divergence around the peak of the Tech Bubble in March 2000

- Tech peaked in March 2000

- Telcos started falling post-March 2000. The tech bubble hurt the telcos sector burst.

- Healthcare showed reliance against the volatility and trended up.

- Utilities remained stable

- Consumer Staples offers essential products that keep demand steady. We can see the uptrend it remained.

- SPX500 of course, represents the broader US market, which got hurt by the Tech Bubble

There was a shift from high-risk tech stocks to more stable and defensive sectors. The divergence between Tech and others like Healthcare and utilities shows this rotation.

Sectors such as Consumer Staples and Utilities are safe havens during market downturns. The impact of the Tech bubble burst shows how important it is to have a diverse portfolio.

If you're afraid of the AI bubble collapsing, I recommend buying Healthcare ETFs. I am doing that together with the Energy sector (such as XLE); however, I have to buy different ETFs because I am European, and there are regulations for ETFs (long story).

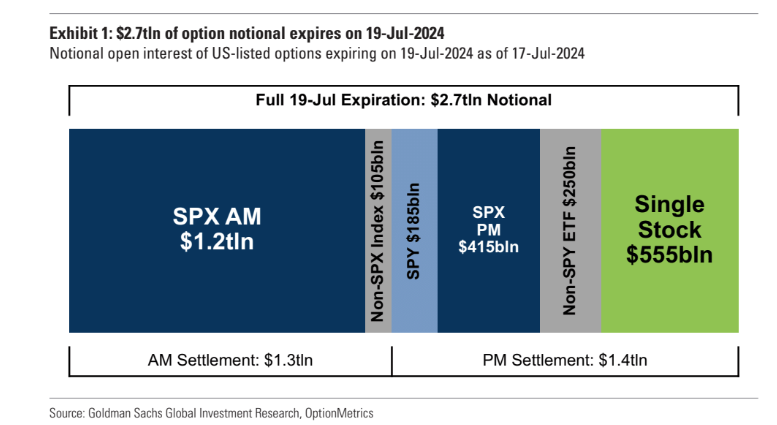

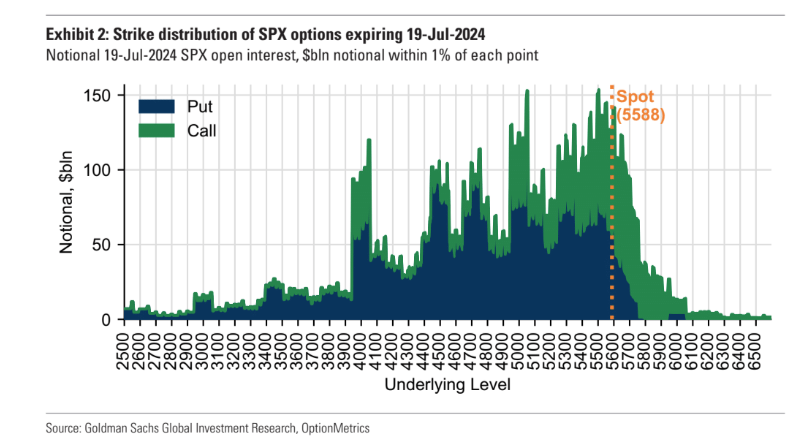

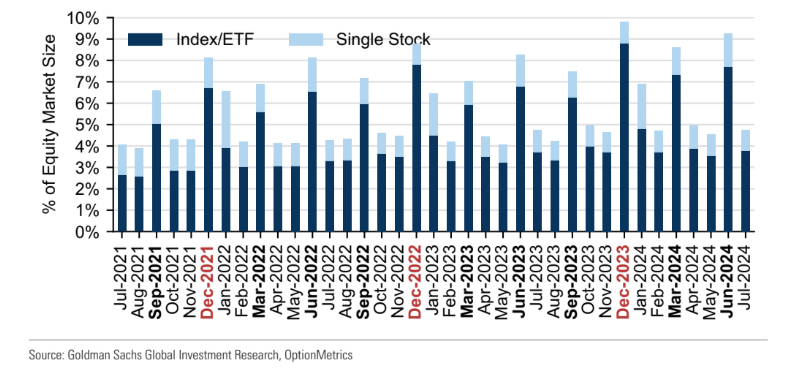

Options Expiration

This Friday will set the record for the largest July option expiration. A rebound in the volumes of index and ETF options is driving this. Over $2.7 trillion in notional options exposure, including $555 billion in single stocks, is set to expire.

- SPX AM ($1.2 trillion)

- Non-SPX Index ($105 billion)

- SPY ($185 billion)

- SPX PM ($415 billion)

- Non-SPY ETF ($250 billion)

- Single Stock ($555 billion)

The total expiration is split into AM and PM settlements of $3.1 trillion and $1.4 trillion, respectively.

There was a high volume because July is usually one of the smaller expiration months. The largest expirations usually happen in January, March, June, September, and December. This July's unusually high volume shows the increase in trading activity of both index and ETF options.

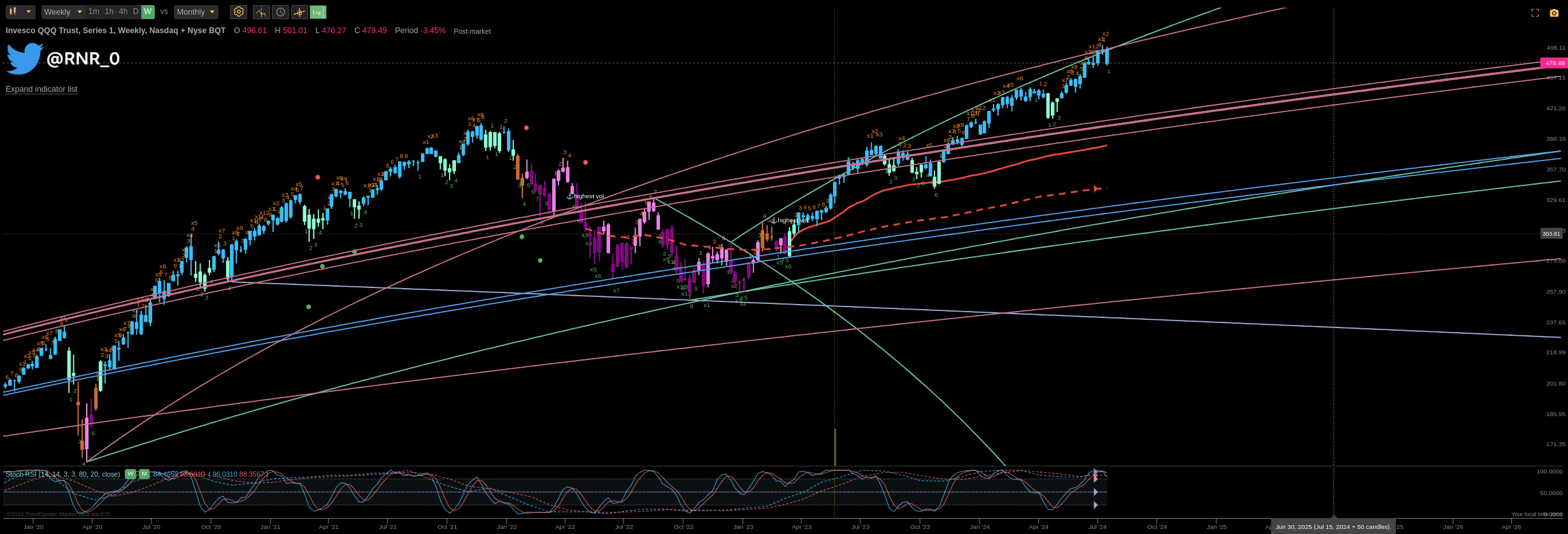

Chart of the QQQ weekly chart

Monthly